Weekly Update | April 12, 2024

Let’s hop straight into five of the biggest developments this week.

1. NZ Official cash rate held steady at 5.50%

The Committee agreed to leave the Official Cash Rate (OCR) at 5.50%. They stated that the NZ economy continued to evolve and requires constant monitoring. Current SPI remains above the Committee’s 1 to 3 percent target range so need constant monitoring.

2. US CPI rises 0.4% m/m vs expectations of 0.4%

CPI in the US increased 0.4 percent in March on a seasonally adjusted basis, the same increase as in February, the U.S. Bureau of Labor Statistics reported earlier this week. Over the last 12 months, all items index increased 3.5% before seasonal adjustment. Shelter and gasoline were the major contributors. This release continues to demonstrate that inflation needs to be monitored closely to avoid an unwanted spike.

3. US FOMC meeting minutes inconclusive

On Thursday the US Federal Reserve released their FOMC meeting minutes which were somewhat mixed. Commentary discussed that inflation had dropped and was moving in the right direction, however, did state that more work still needs to be done. The commentary from the Fed has been relatively consistent over the last year, as they continue to refer to the path of rate hikes being data dependent.

4. USD Core PPI m/m steady at 0.2%

US Producer Price Index for rose 0.2% in March, seasonally adjusted, the U.S. Bureau of Labor Statistics reported this week. Final prices moved up 0.6% in February and 0.4% in January. This data continues to show that input prices have softened, which has assisted in the fight against inflation.

5. Chinese CPI y/y 0.1%

China’s consumer prices barely increased from a year earlier last month as they came in at 0.1% y/y. Industrial prices continued to slump as well, as they were reported at -2.8% vs -2.8% expected. This underscores the deflationary pressures that remain a key threat to the economy’s recovery.

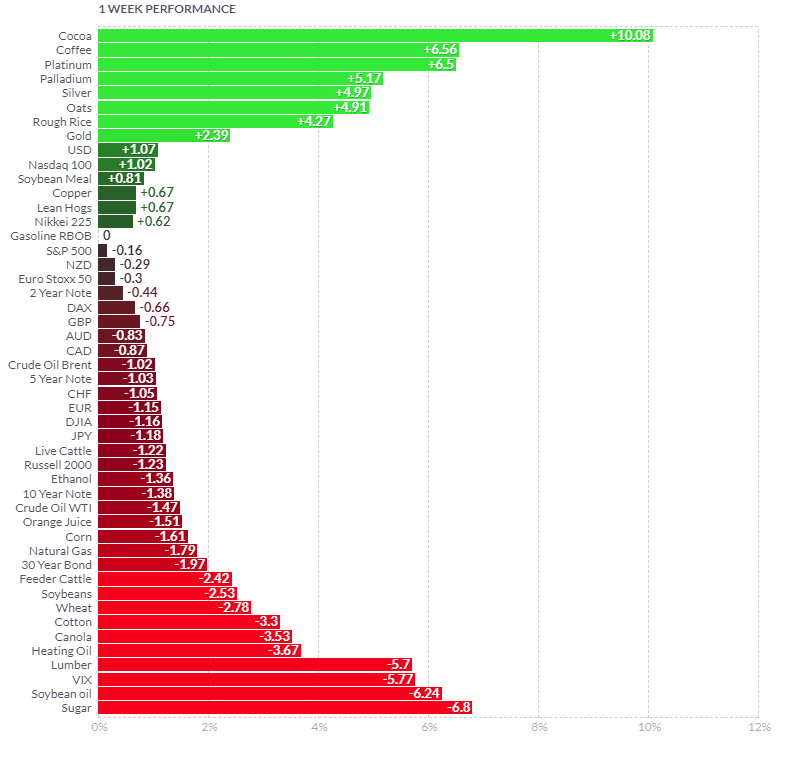

As per usual, below shows the performance of a range of futures markets we track. Some of these are included within the universe of our multi-strategy hedge fund.

Outside of cocoa, this week has seen many new trends develop in global futures markets. Precious metals have experienced a period of solid performance as Silver, Platinum, Palladium and gold all leading the charge. Sugar, Soybean oil and lumber all down on seasonality and their relationship to consumer sentiment and housing starts. The trend in coffee has been positive and is following on from the super trend in Cocoa. The VIX reversed course from last week, as it was down -5.77%.

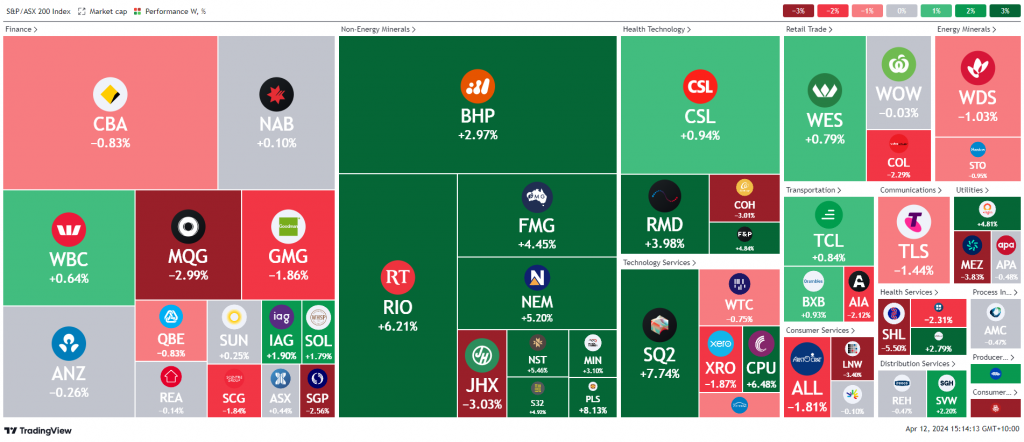

Here is the week’s heatmap for the largest companies in the ASX.

Another mixed week on the ASX with pockets of the market rebounding, while other sectors selling off or consolidating. Materials, SQ2 and Healthcare were the outstanding performers over the course of the week. Aided by the solid rebound in iron ore prices, BHP, RIO and FMG were all up >2.9%. The banks were mixed as a response to global CPI and Monetary Policy statements. PLS, NST, MIN and S32 were all very solid, led higher by a surge in their underlying commodity prices.

Another mixed week on the ASX with pockets of the market rebounding, while other sectors selling off or consolidating. Materials, SQ2 and Healthcare were the outstanding performers over the course of the week. Aided by the solid rebound in iron ore prices, BHP, RIO and FMG were all up >2.9%. The banks were mixed as a response to global CPI and Monetary Policy statements. PLS, NST, MIN and S32 were all very solid, led higher by a surge in their underlying commodity prices.

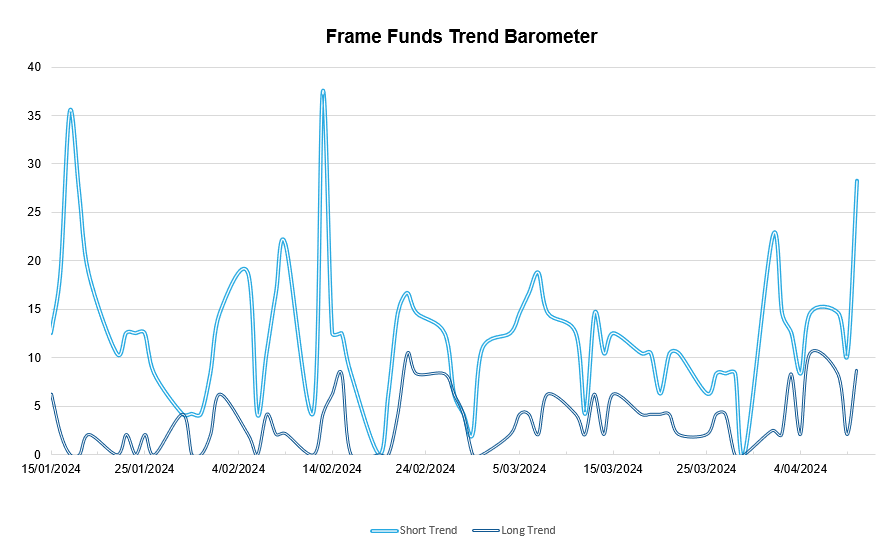

Below shows our proprietary trend-following barometer which captures the number of futures contracts within our universe hitting new short and long-term trends.

Please reach out if you’d like to find out more about how our quantitative approach captures the price action covered above, or if you would like to receive these updates directly to your inbox, please email admin@framefunds.com.au.