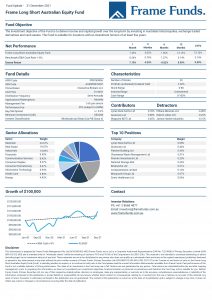

Units of the Frame Long Short Australian Equity Fund increased +7.45% in December. Comparatively the S&P/ASX200 rose +2.60% for the month.

December saw the Omicron variant spread rapidly across Australia, as New South Wales, Victoria and Queensland pressed ahead with reopening plans. Markets trended higher despite this, as policy makers continued to push a ‘living with the virus’ mentality. RBA Governor Lowe said the central bank has adopted a ‘wait and see’ mindset with regard to tapering and interest rate increases. The market will have to wait until the February meeting to see if asset purchases will continue, slow or completely stop.

We began the month exiting positions in Oil Search Ltd (ASX: OSH) as the oil price fell significantly, and Pilbara Minerals (ASX: PLS) as it entered an extreme overbought state. These positions were replaced with GrainCorp Ltd (ASX: GNC) and Sonic Healthcare Ltd (ASX: SHL). Sonic was primed to benefit from increased COVID-19 cases in the community, while GrainCorp is positioned to profit from continuing supply chain squeezes. We also opened a position in James Hardie Industries (ASX: JHX) as strong demand for building materials looks set to continue.

Top equity contributors were Lynas Rare Earths Ltd (ASX: LYC), GrainCorp Ltd (ASX: GNC) and Waypoint REIT Ltd (ASX: WPR). They contributed +0.78%, +0.68% and +0.45% respectively. Lynas continued its stellar performance, confirming the rare earth theme is still very much in play. Waypoint benefited from higher inflation and interest rate expectations, while GrainCorp rose off the back of higher commodity prices caused by supply chain issues. Active trading strategies generated +3.67% for the month.

Largest detractors were Pilbara Minerals Ltd (ASX: PLS), Kalium Lakes Ltd (ASX: KLL) and James Hardie Industries (ASX: JHX) which detracted -0.48%, -0.23% and -0.15% respectively. Pilbara was caught in some volatility at the start of the month, while Kalium Lakes fell after they downgraded CY2022 harvest guidance. James Hardie continued to consolidate near highs. Materials continues to be the highest weighted sector at 23.67% with utilities the only sector where we have no exposure.

At the conclusion of the month, the Fund held 22 investments.

The full report can be downloaded by clicking the image below.