After the most recent FOMC meeting, we have seen numerous changes to forward probabilities within the fixed income market.

This article aims to provide investors with an update on what changes have happened in the fixed income market, and how markets are viewing the next 9 months of this interest rate cycle.

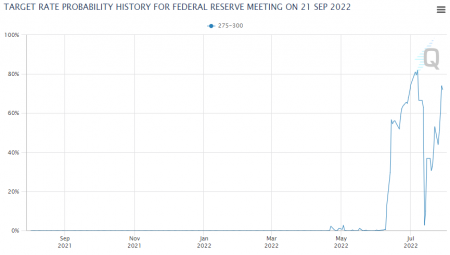

At the September meeting, expectations for a 50bps increase is unchanged

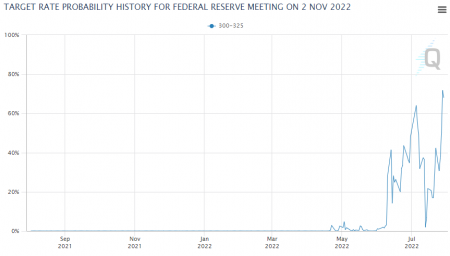

For the November meeting, another 25bps increase has 68% odds of happening, this would bring the target range to 3.00% – 3.25% – no real change here

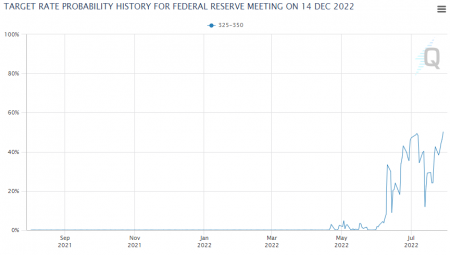

For the December meeting, another 25bps increase has 50.15% odds of happening, this would bring the target range to 3.25% – 3.50% – an increase here

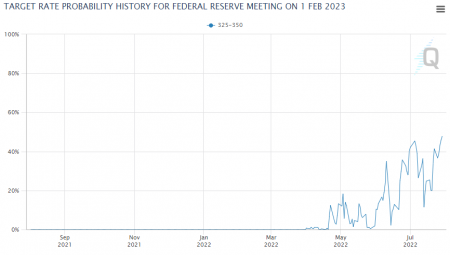

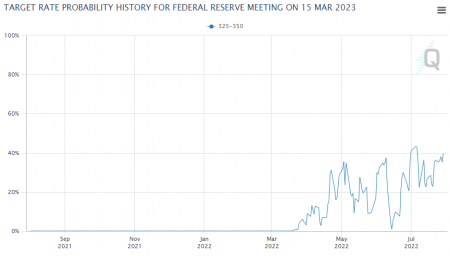

When we look at the February meeting – odds of a hold are currently at 47.8%

When we look to the March meeting expectations are for a hold to rates once again

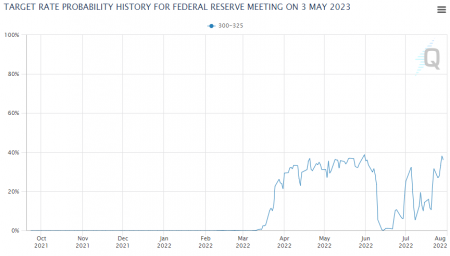

But then when we look to May, it is showing that the market thinks there is a 36% chance of a cut of 25%

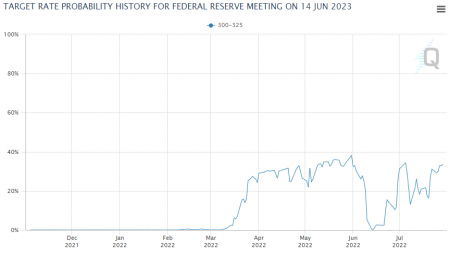

And then when you look forward to June, markets are pricing that there will be a hold on rates once again

Ultimately the market is saying that they are going to continue to increase rates over the next three meetings by 50bps and then 25bps, and then at the December meeting, increase by a further 25bps.

After this, and into next year, the market is currently pricing that rates will either be held or will cut.

What does this mean for portfolio positioning?

We view these changes to the forward pricing of interest rates markets as a direct indication that investors are anticipating that US growth is going to slow later this year and into early next year, and that in response to this slowing growth, the US Federal Reserve is going to reduce interest rates.

This is the same game plan that the US Federal Reserve has used since the GFC. The problem with this game plan is that if inflation continues to stay at elevated levels over the next 6 months, and does not revert to their targeted 2% level, this market pricing is off.

Summary

By looking at this information, we are able to understand why equity markets rallied last month. Participants seem to be viewing where we are currently, as getting close to the top of this interest rate cycle. Because equity markets are forward looking, participants have looked into the future and see the end of this cycle, and that the Fed is starting to move in the other direction.