Weekly Update | November 03, 2023

Let’s hop straight into five of the biggest developments this week.

If you’d prefer to watch this update, rather than read it, please click below.

1. Chinese manufacturing PMI fell to 49.5

Weaknesses in Chinese industrial output are becoming endemic and far-reaching. The manufacturing PMI survey report for October was below expectations at 49.5, dampening optimistic market expectations that September’s uptick figure of 50.2 would be retained. This effectively threw Chinese manufacturing back into contraction, thereby highlighting the stinging demand shortfalls the country is currently grappling with.

2. Japanese interest rates remained static at – 0.10%

The BOJ held fast on its longstanding monetary policy, leaving interest rates unchanged at – 0.10%. This was entirely expected, as the BOJ strives to retain accommodative monetary policy to grow the Japanese economy. Tacit signs of flexibility are however beginning to emerge after the decision to unpeg the central bank’s yield curve control framework from 1% to 1.25%. The tweak brought renewed focus into Japan’s consistently uneventful and predictable monetary policy.

3. New Zealand unemployment rate rose to 3.9%

New Zealand’s labour market deteriorated slightly in the third quarter of 2023. The labour market report showed a marked rise in unemployment rate to 3.9% from the previous 3.6%, the highest since Q2 of 2021. The report showed that the participation rate rose which meant the unemployment rate rose naturally. Employment change q/q declined by -0.2% which was the lowest employment change since November 2020.

4. FOMC held interest rates steady at 5.5%

The Fed sat in its hands for a second consecutive meeting to leave interest rates unchanged at 5.5% in line with market forecasts. The overall theme for the pause, according to the minutes, was that the full effects of the previous aggressive tightening program have yet to fully kick into the economy. The central bank is therefore taking its time to observe the previous rate increases work their way into the economy.

5. UK’s BOE held interest rates at 5.25%

The BOE maintained interest rates at 5.25%, however, they did so with a continued hawkish tone. The decision was in line with the overall market consensus. A softening of inflation, a loosening labour market, and weakening economic activity have restrained further tightening. The central bank, however, cautioned that monetary policy would remain restrictive for much longer with its inflation objectives a long way off.

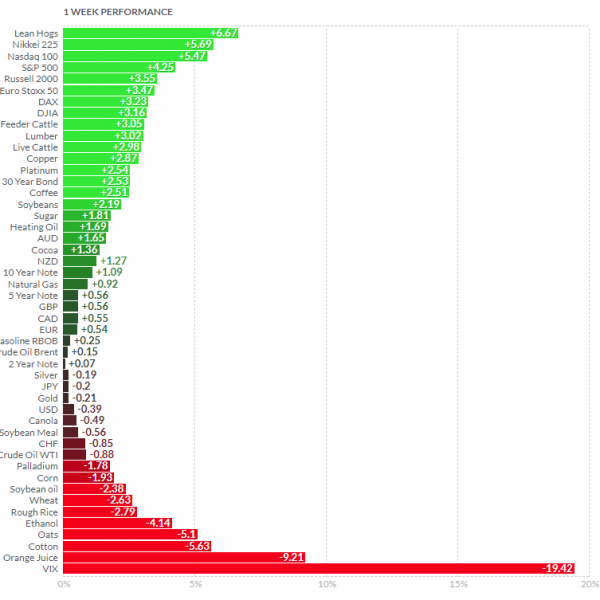

Below shows the performance of a range of futures markets we track. Some of these are included within the universe of our multi-strategy hedge fund.

The VIX plummeted as equity markets rebounded from extremely oversold conditions. This bounce was also caused by most major economies holding interest rates steady. Investors piled into equities with the Nasdaq, Nikkei 225 and S&P 500 all up over +4%. We expect this aggressive snap back, short squeeze cover rally will continue through November, and possibly December. US treasuries rebounded on softer economic data, while copper and iron ore rose. Lean hogs and feeder cattle shot up on rising feed prices and low feed supply. On the other hand, emerging reports of better than expected weather and reduced probability of El Nino phenomena around the world sent orange juice, corn, ethanol, soybean oil, wheat and corn lower.

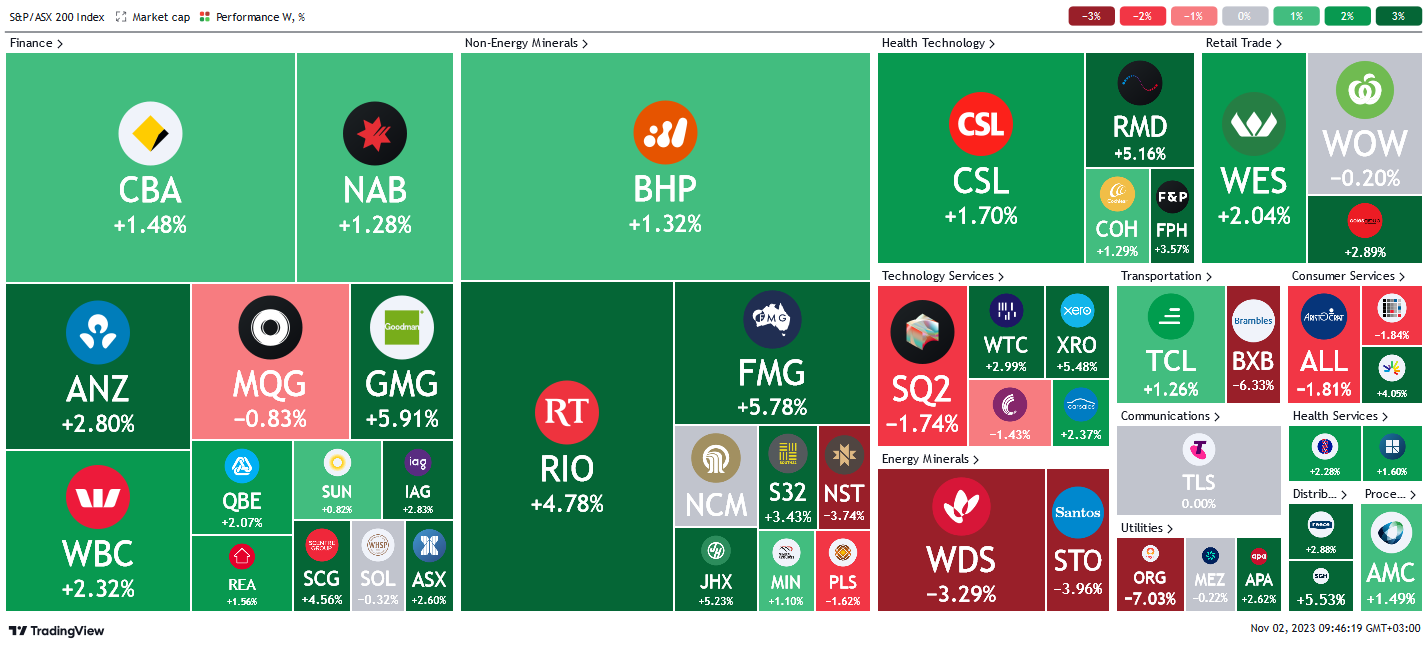

Here is the week’s heatmap for the largest companies in the ASX.

The ASX rebounded this week with healthy gains across most sectors. The financial sector led the rally with nearly all stocks in the green. Goodman group and Scentre Group led the charge on improving demand for commercial spaces. Non-energy miners were equally upbeat. FMG and RIO were the biggest gainers on increased demand for iron ore. NST and PLS continued their slide. NST due to money asset allocations post NCM/Newmont, while PLS dropped on declining Lithium prices. Healthcare tech, retailers and tech services were also up for the week. Energy was the main weak spot, as the crude price (-1%) dragged on WDS and STO.

The ASX rebounded this week with healthy gains across most sectors. The financial sector led the rally with nearly all stocks in the green. Goodman group and Scentre Group led the charge on improving demand for commercial spaces. Non-energy miners were equally upbeat. FMG and RIO were the biggest gainers on increased demand for iron ore. NST and PLS continued their slide. NST due to money asset allocations post NCM/Newmont, while PLS dropped on declining Lithium prices. Healthcare tech, retailers and tech services were also up for the week. Energy was the main weak spot, as the crude price (-1%) dragged on WDS and STO.

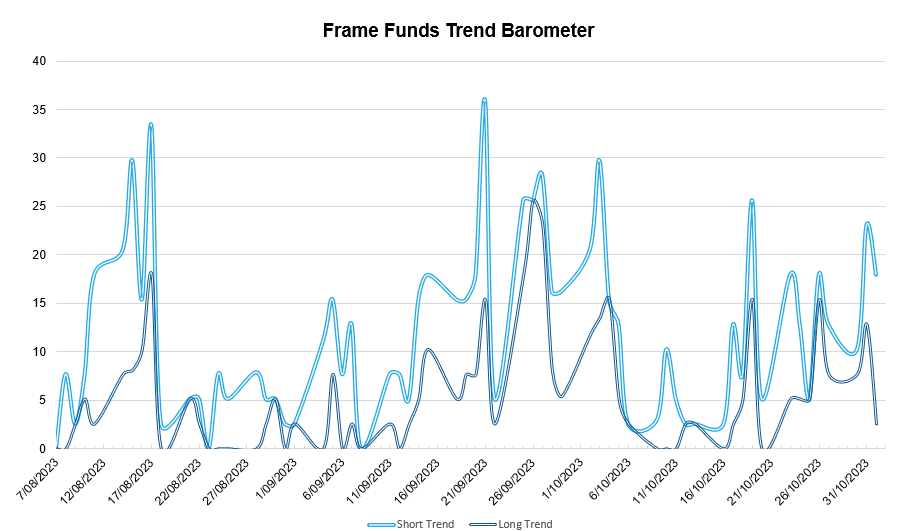

Below shows our proprietary trend-following barometer which captures the number of futures contracts within our universe hitting new short and long-term trends.

*Historically there is a positive correlation between the number of constituents experiencing both short and long-term trends and the performance of the strategy.

Please reach out if you’d like to find out more about how our quantitative approach captures the price action covered above, or if you would like to receive these updates directly to your inbox, please email admin@framefunds.com.au.